Table of Contents

In the United States, safety in finance is often associated with predictability. And very few financial products feel as predictable like fixed deposits, commonly known in the U.S. as Certificates of Deposit (CDs).

You put your money inside.

You earn one fixed interest rate.

You get your principal back at maturity time.

No volatility. No market swings. No anxiety.

On the surface, CDs feel like the responsible choice, especially during uncertain times. They are often recommended to conservative savers, for retirees, and anyone who wants peace of mind.

But safety in appearance does not always equal safety in outcome.

This article explains why those “safe” fixed deposits can quietly become risky over time, not because they lose money outright, but because they fail to protect the things that actually matters: purchasing power, flexibility, and long-term growth.

Why Fixed Deposits Feel So Reassuring

Fixed deposits feel safe because they remove uncertainty.

You know:

- The interest rate upfront

- The maturity date

- The exact dollar amount you will receive

There are no surprises. That certainty feels comforting, specially when markets feel unpredictable.

For many peoples, safety equals to not losing nominal dollars. So long as account balance never goes down, it feels like progress.

But financial safety is not just only about avoiding visible loss. It is also regarding avoiding silent loss.

The Difference Between Nominal Safety and Real Safety

Nominal safety means your dollar amount does not decrease.

Real safety means your money maintains or increases its power of purchase.

Fixed deposits are strong for the first point and they are often weak for the second point.

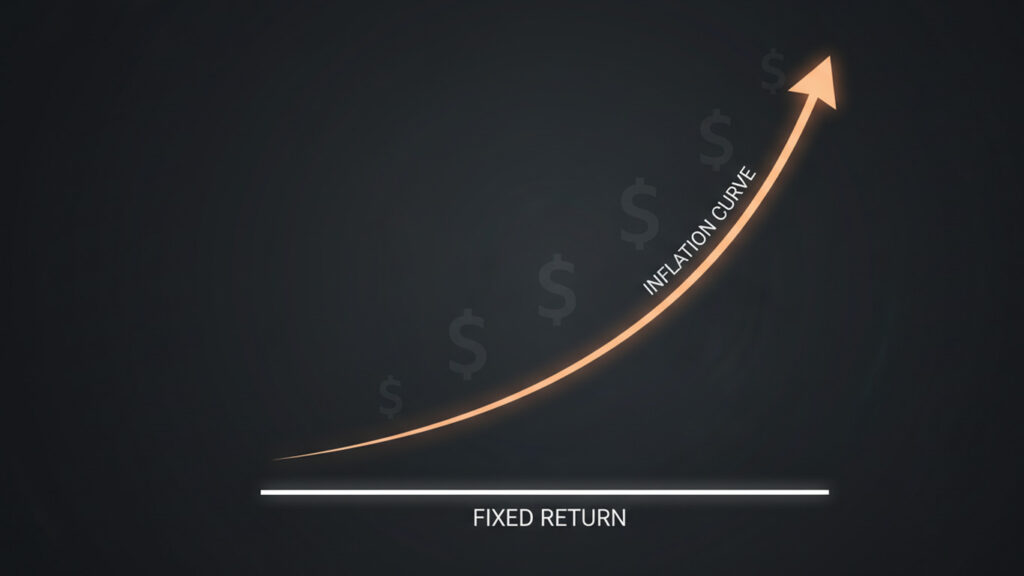

If your CD earns 3 percent annually but the inflation averages 4 percent, your money grows on paper but shrinks in the real terms.

You feel safe. Your future buying power disagrees with this.

Inflation Is the Risk CDs Don’t Protect You From

Inflation is the biggest hidden risk in fixed deposits.

It does not break accounts.

It does not trigger alerts.

It does not feel dramatic.

It quietly increases the cost of everything you buy.

If inflation consistently exceeds the return on your fixed deposit, you are guaranteed to lose purchasing power every year. That loss compounds over time.

This is not a market risk. It is a mathematical certainty.

Why Low Volatility Is Not the Same as Low Risk

Volatility gets labeled as the risk because it feels uncomfortable.

But volatility is a short-term movement. Risk is for the long-term outcome.

A volatile asset can recover and grow over the time.

A stable but low-return asset can permanently lag behind the inflation.

Fixed deposits minimize emotional discomfort but often maximize the long-term opportunity cost.

The absence of volatility does not mean the absence of danger at all.

The Opportunity Cost of Playing It Too Safe

Every dollar placed in a fixed deposit is a dollar not placed elsewhere.

That elsewhere could be:

- Retirement accounts

- Growth assets

- Diversified portfolios

- Inflation-adjusted instruments

The cost of missing these opportunities does not show up as a bill. It shows up as slower wealth accumulation.

Over decades, this missed growth can be larger than any temporary market loss you avoided.

Lock-In Risk: When Safety Reduces Flexibility

Fixed deposits are not just low-return instruments. They are also illiquid.

Once your money is locked in:

- Access is limited

- Early withdrawal penalties apply

- Opportunities cannot be seized easily

If interest rates rise, your money remains stuck at a lower rate.

If an emergency occurs, accessing funds becomes costly.

Liquidity is a form of safety that fixed deposits often sacrifice.

Interest Rate Risk Works Against You

Many people associate interest rate risk with bonds and markets.

But fixed deposits carry interest rate risk too.

When rates rise:

- Existing CDs become less attractive

- Your locked rate becomes outdated

- New deposits earn more than your money

This creates a hidden disadvantage. You did nothing wrong, yet your money underperforms simply because it is trapped.

Safety should not mean being stuck.

Why CDs Feel Safer Than They Actually Are

Psychologically, CDs check all the right boxes:

- Guaranteed returns

- Clear timelines

- No visible losses

Markets, on the other hand, feel chaotic.

But this comfort often leads to over-allocation. People put too much money into fixed deposits because they feel safe, not because they are optimal.

Over time, safety turns into stagnation.

The Long-Term Impact on Retirement

Retirement planning exposes the weakness of fixed deposits clearly.

Retirement is a long-term goal. Inflation is relentless over long periods.

Money that grows slower than inflation:

- Buys less healthcare

- Buys less housing

- Buys fewer years of comfort

Using fixed deposits as a primary long-term strategy increases the risk of outliving purchasing power, even if the account balance looks stable.

Safety Can Become a False Sense of Progress

This is the most dangerous part.

With fixed deposits:

- Balances increase every year

- Statements look positive

- There is no emotional stress

This creates the illusion of progress.

But if real growth is absent, the progress is cosmetic. You are moving forward numerically while standing still economically.

False progress delays course correction.

When Fixed Deposits Do Make Sense

Fixed deposits are not useless.

They make sense for:

- Short-term goals

- Emergency funds

- Capital preservation needs

- Reducing volatility in a broader strategy

The risk appears when they are mistaken for long-term growth solutions.

Safety is a role, not a strategy.

The Real Risk Is Not Losing Money, It Is Losing Time

Time makes big every financial decision, you see.

Low return compounded over many decade make the big-big gap between what could have been and what is actually there.

The real danger for fixed deposit is not they are failing very big. It is that they are succeeding average only for much too long time.

Average performance, when it is compounded, it becomes very costly matter.

Why Conservative Choices Can Be Aggressively Risky

Playing it safe feels conservative. But in a world where inflation exists, safety without growth is aggressive risk.

It risks:

- Falling behind silently

- Reducing future options

- Creating dependency on income later in life

True financial safety balances stability with growth.

The Question That Changes Perspective

Instead of asking:

“Is this safe?”

The better question is:

“What will this money be worth in real terms 10 or 20 years from now?”

That question exposes risks that stability hides.

Final Thought

Fixed deposits promise certainty. And they deliver that thing.

What they do not promise, and often fail for delivering, that is progress.

Safety that ignores inflation, the opportunity cost, and time is incomplete safety?

Real financial security comes not from avoiding movement, but from choosing the correct kind of movement.

When you understand this fully, safety stops being about comfort and starts being about the outcomes only.

Related Analysis

How to Build a Monthly Budget Using the 50/30/20 Rule (With Real Examples)

February 13, 2026

The Psychology of Small Expenses: Why Daily Spending Hurts More Than Big Purchases

February 11, 2026

Why Two People With the Same Salary End Up With Very Different Net Worths: A Math-First Breakdown

February 9, 2026

Compounding Is Not Magic: It’s Just Time Doing the Heavy Lifting

February 7, 2026