Table of Contents

When you are taking a loan in the United States, the conversation usually sounds reassuring.

You are told the interest rate.

You are shown a monthly payment.

You are given a term length.

That feels like full disclosure.

But what you are shown is only the surface thing. The most important mechanics of how interest actually behaves, how loan structures work over time, and how small structural choices multiply cost are rarely explained clearly.

This is not because banks are hiding information illegally. It is because the details are complex, uncomfortable, and not required for selling a loan, you see.

This article breaks down what banks rarely explain about interest rates and loan structures, and why understanding these mechanics matters far more than the headline rate.

The Interest Rate You See Is Not the Cost You Pay

Most borrowers focus on the interest rate as if it were the price of the loan.

It is not.

The interest rate is a pricing input, not the final outcome.

Two loans with the same interest rate can produce wildly different total costs depending on:

- Loan structure

- Repayment schedule

- Term length

- Timing of payments

The rate tells you how interest is calculated. It does not tell you how much interest you will actually pay.

Why Monthly Payment Is a Distraction

Banks emphasize monthly payments because they feel practical.

People live month to month. If a payment fits the budget, the loan feels affordable.

But monthly payment hides:

- How slowly principal is reduced

- How long interest keeps compounding

- How much total interest accumulates

A lower payment almost always means a higher total cost.

Banks don’t emphasize this trade-off because it makes loans harder to sell.

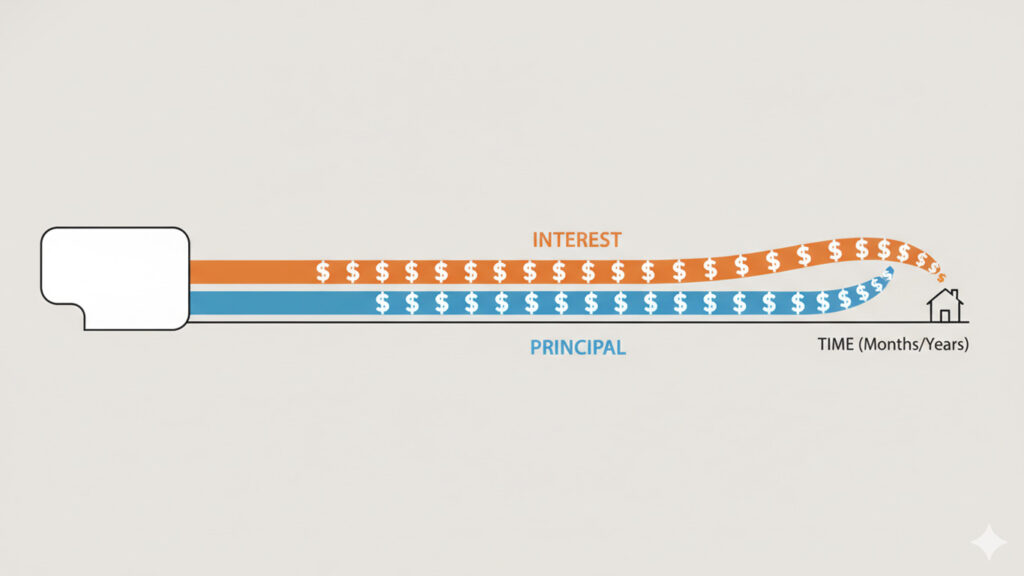

How Amortization Quietly Works Against You

Most consumer loans in the U.S. are amortized loans.

That means:

- Each payment includes interest and principal

- Early payments are interest-heavy

- Principal reduction is slow at first

In the early years of a loan:

- The balance barely moves

- Interest dominates each payment

- Equity builds very slowly

This structure benefits lenders because interest is collected early and reliably.

Borrowers often assume steady payments mean steady progress. The amortization schedule says otherwise.

Why Early Years Matter More Than You Think

The first few years for a loan determine the most of its cost.

If you:

- Choose a long tenure time

- Make only minimum payments

- Avoid prepayments in initial time

Then the interest has maximum possible time for working against you.

Small actions early, like paying slightly higher money or making occasional prepayments, can reduce total interest dramatically. But banks rarely encourage this type of good behavior.

They show the required payment, not the path.

Fixed Rate vs Adjustable Rate Is Not Just About Stability

Fixed-rate loans are marketed as safe. Adjustable-rate loans are marketed as risky.

The reality is more nuanced.

A fixed rate:

- Provides payment stability

- Locks in current rates

- Can become expensive if rates fall

An adjustable rate:

- Starts lower

- Shifts risk over time

- Can increase unpredictably

Banks often frame this as a risk decision. In reality, it is a timing and flexibility decision.

What matters is:

- How long you plan to keep the loan

- How rate changes affect your cash flow

- Whether refinancing is realistic

Without this context, the comparison is incomplete.

APR Is More Important Than the Interest Rate

Banks often advertise the interest rate, not the APR.

APR includes:

- Interest rate

- Fees

- Points

- Certain closing costs

Two loans with the same interest rate can have very different APRs.

APR gives a better picture of the true cost of borrowing, especially for shorter-term loans. Yet it is often buried in fine print.

The rate sells the loan. The APR reveals it.

Compounding Works for the Bank First

Interest compounds continuously on outstanding balance, boss.

Till the time your principal amount remains high:

- Interest accumulates faster

- EMI payments remain more interest-heavy

- Total cost keeps on growing, na?

Banks benefit maximum when the loans stay open longer period and balances remain high, sir.

For this reason, long loan terms and minimum payments are promoted heavily, only.

Compounding is not neutral thing. Structure decides whom it favors, always.

Why “Low Interest” Can Still Be Expensive

A loan can have a relatively low interest rate and still cost a lot.

Why?

- Long term length

- Slow principal reduction

- High starting balance

A low rate applied for a long time can produce more interest than a higher rate applied briefly.

Duration often matters more than rate.

Interest Is Calculated on Balance, Not Effort

Many borrowers feel much frustrated when they have been “paying since years” and still they owe big large amount.

That frustration comes because of not understanding how the interest works.

Interest does not care how much long time you have been paying.

It only cares regarding how much principal amount remains pending.

If the balance stays high, the interest also stays high.

Effort does not reduce interest. Balance reduction does the needful.

Why Refinancing Often Resets the Clock

Refinancing can lower payments or rates, but it has a hidden cost.

When you refinance:

- The amortization schedule restarts

- Interest-heavy years begin again

- Total interest may increase despite lower rates

Banks emphasize the lower payment. They rarely emphasize the reset.

Refinancing can help, but only when the full timeline is considered.

Loan Structures Are Designed for Predictability, Not Speed

Banks value predictability.

Fixed payments over long terms:

- Reduce default risk

- Create steady cash flow

- Maximize interest collection

Borrowers value speed and efficiency.

These goals are not aligned.

Loan structures are optimized for the lender’s risk model, not for minimizing your total cost.

Why Banks Don’t Explain This Clearly

Explaining loan mechanics thoroughly would:

- Slow down decisions

- Raise uncomfortable questions

- Reduce loan acceptance rates

Complexity works in favor of simplicity in sales.

Banks are not required to teach financial literacy. They are required to disclose numbers. Disclosure is not the same as understanding.

The Cost of Not Understanding Structure

When borrowers do not understand loan structure:

- They over-focus on rates

- They under-estimate total cost

- They delay principal reduction

- They accept unnecessary interest

The result is not immediate harm. It is long-term drag.

What Actually Matters More Than the Rate

The most important factors in a loan are:

- Total interest paid

- Speed of principal reduction

- Term length

- Flexibility without reset

The interest rate is just one piece of a larger system.

Optimizing only the rate while ignoring structure is like optimizing fuel price while ignoring mileage.

The Question Banks Don’t Encourage

Instead of asking:

“What’s the interest rate?”

The better question is:

“How much interest will I pay in total if I follow this structure exactly?”

That question changes everything.

Final Thought

Banks explain that which they are required to explain.

They do not explain that which will make borrowing uncomfortable for you, naturally.

Interest rates are easy for comparison. Loan structures, they are not easy.

But the structure determines the final outcome, naturally.

When you understand how interest really behaves and how loan mechanics quietly shape the cost, borrowing stops being confusing and starts being strategic, naturally.

Clarity does not eliminate the debt. But it prevents unnecessary debt, please do the needful.

Related Analysis

How to Build a Monthly Budget Using the 50/30/20 Rule (With Real Examples)

February 13, 2026

The Psychology of Small Expenses: Why Daily Spending Hurts More Than Big Purchases

February 11, 2026

Why Two People With the Same Salary End Up With Very Different Net Worths: A Math-First Breakdown

February 9, 2026

Compounding Is Not Magic: It’s Just Time Doing the Heavy Lifting

February 7, 2026