Table of Contents

At first glance, salary is feeling like the ultimate financial scorecard. If two people are earning the same amount, they should logically end up in roughly the same financial position. Yet real life is consistently proving otherwise.

You may be earning exactly the same salary as a colleague, friend, or neighbor, but years later the financial gap between you can be feeling enormous. One person is having assets, flexibility, and peace of mind, while the other is feeling stuck despite earning well. This difference is rarely caused by luck, intelligence, or background only. It is almost always the result of mathematics quietly compounding over the time.

This article is breaking down why two people with identical salaries are ending up with very different net worths, using numbers and timelines instead of just opinions or motivation talk.

Salary Is a Starting Point, Not the Destination

Salary is representing income. Net worth is representing accumulation.

They are connected, but they are not the same thing only.

Net worth is being calculated as what you are owning minus what you are owing. Salary only affects how fast money is flowing through your hands. It is not determining how much stays, how it is growing, or how it is compounding.

Two people can be earning the same amount for decades and still end up with completely different financial outcomes because salary is measuring effort, while net worth is measuring structure and consistency.

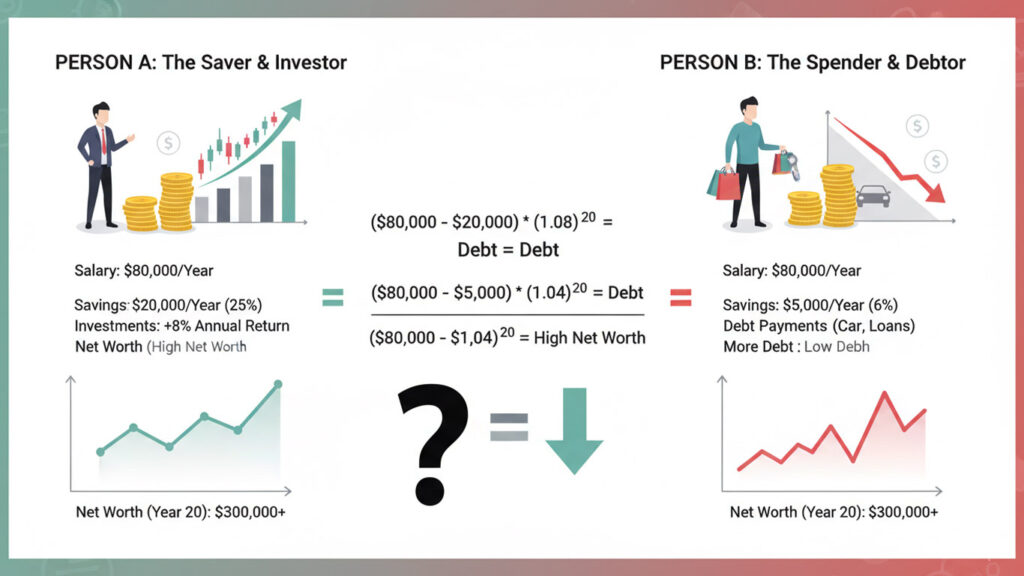

Meeting Two People With the Same Income

Let us imagine two individuals who are looking identical on paper.

Both are earning the same annual salary.

Both are starting their careers at the same age.

Both are receiving similar raises over time.

Both are living in the same city with comparable expenses.

There is no advantage built into the system for either one.

Yet after twenty years, their net worths are nowhere close.

The reason is lying in four invisible variables that salary alone is not showing.

Variable Number One: Savings Rate

Savings rate is the percentage of income that is actually staying with you.

Suppose both individuals are earning $60,000 per year.

Person A is saving 10 percent of income.

Person B is saving 30 percent of income.

Nothing else is changing.

Person A is saving $6,000 per year.

Person B is saving $18,000 per year.

After ten years, ignoring returns, Person A has saved $60,000 while Person B has saved $180,000. The salary was identical same-to-same, but the base capital is already three times larger for one person.

This gap is existing before investing, before inflation, before market returns. It is purely behavioral mathematics.

Savings rate is determining how much money even gets the opportunity for growing.

Variable Number Two: What Is Happening to the Saved Money

Saving money is only half the equation. Where that money is sitting is determining whether time is working for or against you.

Person A is keeping savings mostly idle or in low-yield instruments. The money is feeling safe, but it is growing slowl.y

Person B is investing consistently for long-term growth.

Over twenty years period, the difference is becoming very dramatic.

Money that is compounding is not growing in a straight line path. It is accelerating. The later years are contributing more growth than the earlier ones, even if contributions are staying the same.

This is why two people can save consistently, still one is seeing momentum while the other one is feeling stuck. Compounding is rewarding patience, not effort.

Variable Number Three: Inflation, the Invisible Tax System

Inflation is quietly reducing purchasing power every year. Even modest inflation is eroding money that is not growing fast enough.

If inflation is averaging five percent annually, money that is earning less than that is losing real value. This loss is not feeling painful in a single year, but it is compounding over decades.

Person A is focusing on stability and avoiding volatility.

Person B is focusing on preserving long-term purchasing power.

Years later, Person A is discovering that saved money is buying far less than expected, while Person B’s investments have adjusted for inflation over time period.

Inflation is not announcing itself. It just keeps working silently.

Variable Number Four: Debt Structure and Interest Calculation

Two people can be borrowing the same amount of money and still they are experiencing very different outcomes.

Person A is choosing longer loan tenures because the monthly payment is feeling comfortable.

Person B is focusing on minimizing total interest paid, even if monthly payments are slightly higher.

Over time, Person A is paying significantly more interest to the lenders. Person B is reducing interest leakage and redirecting that money toward assets.

The difference is not visible in the monthly budgets. It is becoming obvious only after years have passed.

Interest is either draining future wealth or accelerating it. Structure is deciding which side you are standing on.

Time Is the Ultimate Multiplier Factor

One of the major reasons net worth diverges is the factor of timing.

Money which is investde early in a career is having far more impact than money invested later, even if later contributions are larger. The early years are carrying disproportionate weight because compounding needs time to breathe.

Delaying investing by five or ten yeras is often requiring dramatically higher contributions later just to do the catch up. This is creating a situation where two people with the same lifetime income are ending up in completely different financial realities.

Time is not forgiving the indecision.

Lifestyle Inflation Is Changing Everything for Sure

When the income is increasing, spending often increases automatically.

Person A is upgrading lifestyle with every raise. Expenses are growing alongside income, keeping the savings rate flat only.

Person B is increasing savings first and upgrading lifestyle selectively.

Both are feeling comfortable. Only one is building flexibility.

Lifestyle inflation is not feeling like a mistake because nothing is breaking immediately. Its cost is invisible and is showing up as lost future options rather than present discomfort.

Net Worth Is Being a Lagging Indicator

This is the area where many people are getting confused.

Net worth is reflecting decisions which were made years ago, not recent effort.

When someone appears financially ahead, you are seeing the result of long-term consistency, not just current income. When someone is struggling despite earning well, it usually reflects delayed compounding, inefficient cash flow, or excessive interest leakage from the past time.

Net worth is not a judgment of intelligence or hard work. It is simply a record of mathematics applied over a period of time.

Why This Thing Is Feeling Unfair

It is feeling unfair because salary is visible and progress is delayed.

Two people can be working equally hard and still see very different outcomes because math is compounding quietly. There are no alerts, no warnings, and no emotional signals coming when things are drifting off track.

The difference is rarely dramatic in the beginning. It is becoming dramatic only when sufficient time has passed.

The Main Core Insight

The gap between people having the same salary is rarely about the income.

It is about how much is being saved, how early investing is starting, how inflation is being handled, and how debt is being structured.

Salary is starting the engine.

Behavior is choosing the direction.

Mathematics is deciding the destination.

One Final Thought

Financial outcomes are not sudden events like that. They are slow, cumulative processes.

Small decisions repeated consistently are creating massive differences over time period. The same math that is working against careless habits is working powerfully in favor of disciplined ones.

When you are understanding this thing, comparison is becoming pointless. Progress is becoming measurable. And financial clarity is shifting from emotional feelings to intention.

Related Analysis

How to Build a Monthly Budget Using the 50/30/20 Rule (With Real Examples)

February 13, 2026

The Psychology of Small Expenses: Why Daily Spending Hurts More Than Big Purchases

February 11, 2026

Compounding Is Not Magic: It’s Just Time Doing the Heavy Lifting

February 7, 2026

How Taxes Change Your Real Income More Than Your Salary Slip Shows

February 6, 2026