Table of Contents

Most people do not decide not to invest. They decide they will do it later.

Later, when income is on the higher side.

Later, when debt is lower side.

Later, when the life feels more settled.

A five-year delay feels harmless only. It sounds short. It feels recoverable, no? After all, what difference five years can really make in a 30- or 40-year service period?

The answer, when you look at the mathematics, is uncomfortable only.

This article shows what actually happens when investment is delayed by just five years only, using proper timelines, compounding logic, and real-world U.S. assumptions. No hype is there. No fear tactics is applied. Just the numbers are doing what numbers do.

Why Five Years Feels Like Nothing

Five years feels small because for imagining, it is an easy matter.

You can picture clearly your life five years back. That thing makes future feel near and controllable. You assume you can make up for any lost time by investing more later on.

The big problem is that compounding does not treat the time evenly, you see.

Initial years matter more than the years coming later, even if the dollar amounts you are investing later are very much larger.

This is not just an opinion, no. It is a proper mathematical property of exponential growth.

Two Identical People, One Small Difference

Let’s imagine two people.

Both:

- Earn the same income

- Invest in the same assets

- Earn the same long-term average return

- Stay invested until retirement

The only difference is timing.

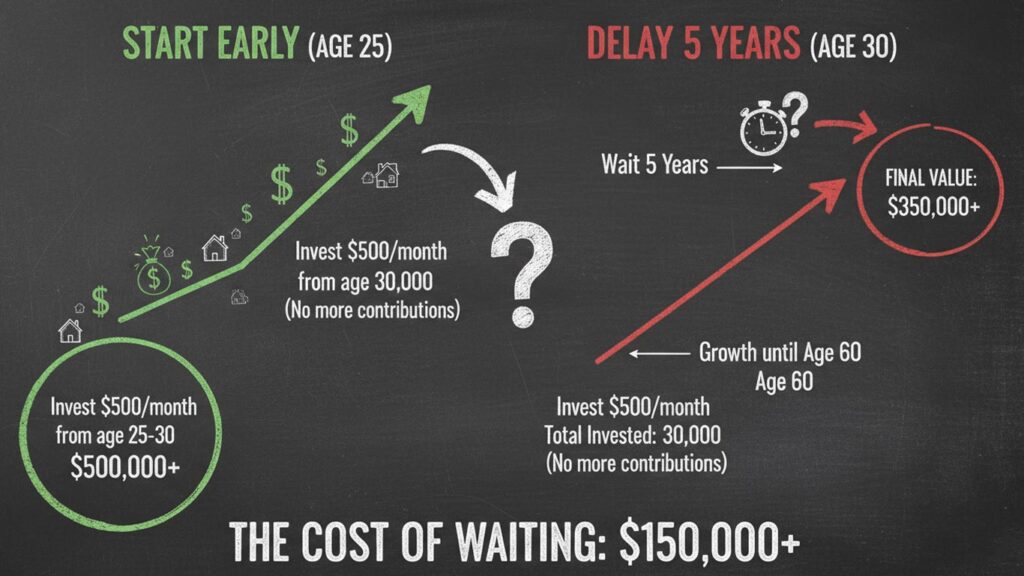

Person A starts investing at age 25.

Person B starts investing at age 30.

Everything else is identical.

That five-year gap is the only variable.

The Core Mechanism: Compounding Needs Time, Not Effort

Compounding rewards money that stays invested the longest.

Early contributions have more time to:

- Earn returns

- Earn returns on returns

- Multiply without additional effort

Later contributions work harder but have less time.

This is why delaying investing creates a disadvantage that is difficult to erase, even with higher contributions later.

A Simple Timeline Illustration

Assume both individuals invest the same amount every year once they start.

Person A invests from age 25 to 65.

Person B invests from age 30 to 65.

Person A invests for 40 years.

Person B invests for 35 years.

That is a difference of just five years.

But those five years sit at the most powerful point on the timeline, the beginning.

Why Early Dollars Are the Most Valuable

The first dollars invested do not grow the fastest immediately. They grow the longest.

Money invested at 25 has 40 years to compound.

Money invested at 30 has 35 years.

Money invested at 40 has 25 years.

The difference is not linear. It accelerates over time.

This is why early investing feels slow at first and explosive later. The growth curve bends upward, not outward.

When you delay, you miss the base of that curve.

The Catch-Up Myth

Most people assume they can catch up later by investing more.

In theory, this is true.

In practice, it is difficult.

To match the outcome of early investing, delayed investors must:

- Invest significantly higher amounts

- Do so consistently

- Maintain discipline for decades

Life rarely cooperates perfectly.

Higher income later often comes with:

- Higher lifestyle costs

- Family responsibilities

- Career uncertainty

- Health considerations

The ability to invest aggressively later is not guaranteed.

What Happens When You Try to Compensate

When investing starts late, people often respond by:

- Taking higher risk

- Chasing returns

- Increasing contribution stress

This adds volatility and emotional pressure.

Early investors can afford to be patient. Late investors often feel rushed.

Time creates margin. Delay removes it.

The Psychological Cost of Delay

Delaying investing does not just reduce numbers. It increases pressure.

When progress depends heavily on future income and performance:

- Mistakes feel larger

- Market downturns feel scarier

- Decisions become emotional

Early investing spreads risk across time. Delayed investing concentrates risk into fewer years.

That concentration makes outcomes less predictable.

Why Five Years Can Mean Hundreds of Thousands of Dollars

Over the very long horizons, compounding magnifies small time differences into very large outcome gaps.

Five years that are missing in the beginning:

- Cannot be replaced by five extra years at the finishing point

- Cannot be fixed by just doing small adjustments

- Cannot be ignored without having the consequence

Those early years act as the multiplier for everything that comes after this.

This is the reason why two persons with identical incomes and the same strategies can retire with dramatically different net worth amounts.

Inflation Makes Delay Even More Expensive

Inflation reduces the real value of money over time.

When investing is delayed:

- Cash loses purchasing power

- Contributions buy less future growth

- Real returns shrink

Early investing helps counter inflation by letting assets grow alongside rising prices.

Delay allows inflation to work uninterrupted.

Why “Waiting for the Right Time” Backfires

Many people delay investing because they are waiting for:

- Market clarity

- Lower risk

- Better opportunities

Markets rarely feel safe in real time.

Waiting often means missing years of participation while inflation and time continue moving forward.

Compounding does not wait for confidence.

The Asymmetry of Time Loss

This is the harsh truth.

You can always add more money later.

You can never add more early years.

Once time is gone, it cannot be purchased, borrowed, or replaced.

This asymmetry is what makes early years disproportionately valuable.

Why This Matters More Than Rate of Return

People obsess over finding better returns.

In reality:

- A modest return with long time often beats a higher return with short time

- Consistency beats optimization

- Time beats timing

Five extra years at an average return often matter more than several extra percentage points earned later.

The Hidden Benefit of Starting Early

Starting early creates optionality.

It allows you to:

- Reduce contributions later if needed

- Take career risks

- Handle market downturns calmly

- Adjust plans without panic

Delay removes that flexibility and forces precision.

Precision is harder than patience.

Final Thought

Delaying investing for five years does not feel dangerous, Sir. This is because the cost is invisible at first glance.

There is no penalty notice. No warning message is coming. There is no immediate regret also.

The cost shows up many decades later, na? It shows as a much quieter outcome than you had expected.

Time is not just one factor in investing, okay? Time is actually the factor itself.

When you understand this point, starting early stops being only about discipline. It starts being about respect for the mathematics calculation.

That much respect compounds quietly, year after year.

Related Analysis

How to Build a Monthly Budget Using the 50/30/20 Rule (With Real Examples)

February 13, 2026

The Psychology of Small Expenses: Why Daily Spending Hurts More Than Big Purchases

February 11, 2026

Why Two People With the Same Salary End Up With Very Different Net Worths: A Math-First Breakdown

February 9, 2026

Compounding Is Not Magic: It’s Just Time Doing the Heavy Lifting

February 7, 2026